Cite this document

(Evaluation report of the JD sports fashion plc Essay, n.d.)

Evaluation report of the JD sports fashion plc Essay. https://studentshare.org/finance-accounting/1869875-evaluation-report-of-the-jd-sports-fashion-plc

Evaluation report of the JD sports fashion plc Essay. https://studentshare.org/finance-accounting/1869875-evaluation-report-of-the-jd-sports-fashion-plc

(Evaluation Report of the JD Sports Fashion Plc Essay)

Evaluation Report of the JD Sports Fashion Plc Essay. https://studentshare.org/finance-accounting/1869875-evaluation-report-of-the-jd-sports-fashion-plc.

Evaluation Report of the JD Sports Fashion Plc Essay. https://studentshare.org/finance-accounting/1869875-evaluation-report-of-the-jd-sports-fashion-plc.

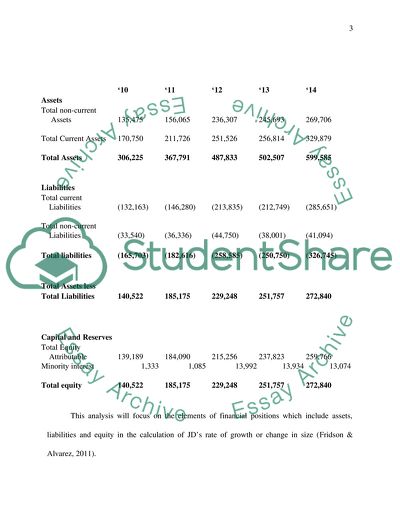

“Evaluation Report of the JD Sports Fashion Plc Essay”. https://studentshare.org/finance-accounting/1869875-evaluation-report-of-the-jd-sports-fashion-plc.