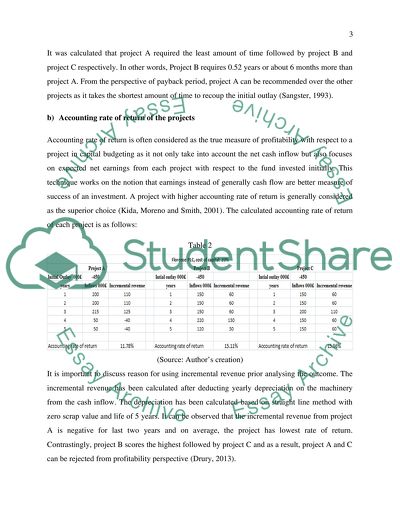

Cite this document

(“Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 words”, n.d.)

Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 words. Retrieved from https://studentshare.org/finance-accounting/1672565-investment-case-study-scenario-florence-plc-is-a-small-listed-company-which-has-recently-raised-450-000-from-a-rights-issue-and-the-directors-are-considering-three-ways-of-using-these-funds

Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 words. Retrieved from https://studentshare.org/finance-accounting/1672565-investment-case-study-scenario-florence-plc-is-a-small-listed-company-which-has-recently-raised-450-000-from-a-rights-issue-and-the-directors-are-considering-three-ways-of-using-these-funds

(Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 Words)

Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 Words. https://studentshare.org/finance-accounting/1672565-investment-case-study-scenario-florence-plc-is-a-small-listed-company-which-has-recently-raised-450-000-from-a-rights-issue-and-the-directors-are-considering-three-ways-of-using-these-funds.

Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 Words. https://studentshare.org/finance-accounting/1672565-investment-case-study-scenario-florence-plc-is-a-small-listed-company-which-has-recently-raised-450-000-from-a-rights-issue-and-the-directors-are-considering-three-ways-of-using-these-funds.

“Florence Regarding Investment Appraisal Essay Example | Topics and Well Written Essays - 1750 Words”, n.d. https://studentshare.org/finance-accounting/1672565-investment-case-study-scenario-florence-plc-is-a-small-listed-company-which-has-recently-raised-450-000-from-a-rights-issue-and-the-directors-are-considering-three-ways-of-using-these-funds.