StudentShare

Our website is a unique platform where students can share their papers in a matter of giving an example of the work to be done. If you find papers

matching your topic, you may use them only as an example of work. This is 100% legal. You may not submit downloaded papers as your own, that is cheating. Also you

should remember, that this work was alredy submitted once by a student who originally wrote it.

✕

Free

The Equilibrium Price and Quantity - Essay Example

Summary

The paper "The Equilibrium Price and Quantity" states that there is a method for calculating the real GDP through the base year price method which is also known as the traditional method. Under this method, each year’s output is valued at the base year’s prices…

- Subject: Miscellaneous

- Type: Essay

- Level: Undergraduate

- Pages: 4 (1000 words)

- Downloads: 0

- Author: beerken

Extract of sample "The Equilibrium Price and Quantity"

Q1. Demand is the amount of a particular economic good or service that a consumer or a group of consumers will want to purchase at a given price (Demand). Supply is the total amount of a good or service available for purchase; along with demand, one of the two key determinants of price (Demand). The equilibrium price and quantity are the respective price and quantity at which the quantity demanded for a product equals the quantity supplied for that product.

Oil is the factor input for gasoline. As the price for a commodity increases, its quantity demanded tends to fall. So in this scenario, should a civil war break out in the Middle East and oil prices rise, the quantity demanded for oil will fall as gasoline producers will find oil expensive. Due to the increase in oil price, cost of production for gasoline producers will rise and so the supply for gasoline will fall as the supply of gasoline has an inverse relationship with the price of oil. This means that if the price of oil increases, the supply of gasoline will fall and if the price of oil decreases, the supply for oil will increase. Diagrammatically expressing, there would be a leftward shift (decrease) in the supply curve (from S to S1) for gasoline and this will bid the price of gasoline up. The equilibrium price changes from P to P1 and as a result, the equilibrium quantity demanded decreases from q to q1.

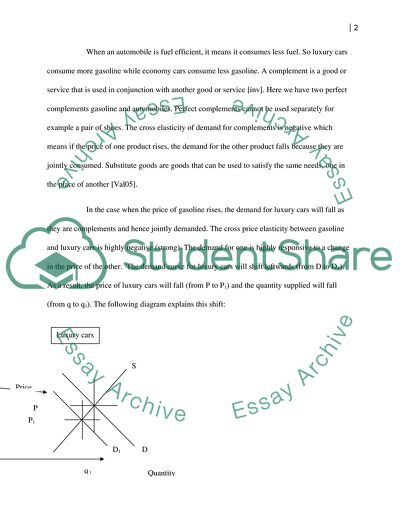

When an automobile is fuel efficient, it means it consumes less fuel. So luxury cars consume more gasoline while economy cars consume less gasoline. A complement is a good or service that is used in conjunction with another good or service (investopedia). Here we have two perfect complements gasoline and automobiles. Perfect complements cannot be used separately for example a pair of shoes. The cross elasticity of demand for complements is negative which means if the price of one product rises, the demand for the other product falls because they are jointly consumed. Substitute goods are goods that can be used to satisfy the same needs, one in the place of another (Piana).

In the case when the price of gasoline rises, the demand for luxury cars will fall as they are complements and hence jointly demanded. The cross price elasticity between gasoline and luxury cars is highly negative (strong). The demand for one is highly responsive to a change in the price of the other. The demand curve for luxury cars will shift leftwards (from D to D1). As a result, the price of luxury cars will fall (from P to P1) and the quantity supplied will fall (from q to q1). The following diagram explains this shift:

Substitutes have a positive cross price elasticity of demand which means that as the price for one product falls, the demand for the other product falls and vice versa for a price increase. So as the price for luxury cars will fall, the demand for economy cars will also fall. There will be a leftward shift of the demand curve for economy cars as now consumers will prefer buying the luxury cars whose price has decreased.

Q2. GDP is the total market value of the nation’s output. Real GDP is GDP which is adjusted for the effects of inflation (Real GDP). First of all, nominal GDP is calculated by adding consumption, investment, government purchases and net exports. The expenditure done by consumers, government, firms, and foreigners on the nation’s output is added. This is known as the expenditure approach for calculating GDP (QuickMBA Economics).

Consumption includes the expenditure on durable and non-durable goods and it is not affected by the estimated value of goods that are imported. Investment comprises of expenditure on fixed assets and inventory. Government purchases are the net amount after subtracting government transfer payments (e.g. welfare, unemployment benefits) from government expenditure. Net exports are exports minus the imports because the purpose of GDP is to find out the value of the domestic output (QuickMBA Economics).

There are three approaches to calculating GDP, each of which gives exactly the same result:

1. Expenditure Approach: Total expenditure on domestics goods and services is added

2. Product Approach: The market value of domestic goods and services is computed

3. Income Approach: This approach works on the principle that one’s expenditure is another’s income. Under this approach, the incomes received by domestic producers are totaled (QuickMBA Economics).

The GDP calculated using the above mentioned approaches is still nominal because it is not adjusted for the effects of inflation. Though the purpose of the price deflator is to take inflation into account, it is different from CPI (Consumer Price Index). It includes government goods, investment goods and exports as opposed to the consumer-centric basket of goods (QuickMBA Economics). It is more rightly called a conversion factor as it converts nominal GDP into real GDP (Nominal GDP, Real GDP and Price). The nominal GDP is divided by the price deflator in order to calculate the real GDP. The nominal GDP happens to be greater than the real GDP because the real GDP is taken in real terms. If the price deflator is not known, then implicit price deflator is calculated by dividing the nominal GDP by the real GDP (QuickMBA Economics).

Another method for calculating the real GDP is through the base year price method which is also known as the traditional method. Under this method, each year’s output is valued at base year’s prices. The real GDP of the base year equals its nominal GDP (Measuring GDP and Economic Growth ). Real GDP is also used for calculating economic growth which is the percentage change in the quantity of goods and services produced year after year (Measuring GDP and Economic Growth ).

Bibliography

Demand. n.d. .

investopedia. n.d. .

Measuring GDP and Economic Growth . n.d. .

Nominal GDP, Real GDP and Price. 7 November 2011. .

Piana, Valentino. Substitute Goods. 2005. .

"QuickMBA Economics." n.d.: http://www.quickmba.com/econ/macro/gdp/.

Real GDP. n.d. .

Read

More

sponsored ads

Save Your Time for More Important Things

Let us write or edit the essay on your topic

"The Equilibrium Price and Quantity"

with a personal 20% discount.

GRAB THE BEST PAPER