StudentShare

Our website is a unique platform where students can share their papers in a matter of giving an example of the work to be done. If you find papers

matching your topic, you may use them only as an example of work. This is 100% legal. You may not submit downloaded papers as your own, that is cheating. Also you

should remember, that this work was alredy submitted once by a student who originally wrote it.

✕

Free

Financial Econometrics - Descriptive Statistics and the Graph of Log Return and Log Prices - Assignment Example

Summary

The paper "Financial Econometrics - Descriptive Statistics and the Graph of Log Return and Log Prices" is a worthy example of an assignment on finance and accounting. In the first part, we are interested in examining the descriptive statistics of the log return and log prices…

- Subject: Finance & Accounting

- Type: Assignment

- Level: Undergraduate

- Pages: 5 (1250 words)

- Downloads: 0

- Author: hoegertwila

Extract of sample "Financial Econometrics - Descriptive Statistics and the Graph of Log Return and Log Prices"

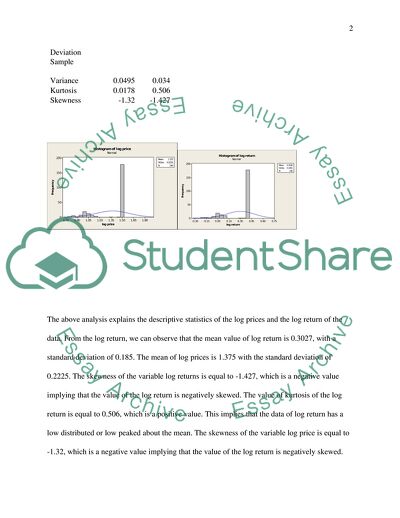

FINANCIAL ECONOMETRIC a) Descriptive statistics and the graph of log return and log prices In the first part, we are interested in examining the descriptive statistics of the log return and log prices. In this analysis, it important to note that excel was used for analysis as it was the most easily available than the pcgive. The descriptive statistic mean, standard deviation, kurtosis, skewness were used to explain the nature of the data in terms of the measure of central tendency and the dispersion of the data. The bar graph of the log price and the log return is obtained

log prices

log return

Mean

1.375

0.3027

Standard Error

0.0144

0.0119

Median

1.5

0.4055

Mode

1.5

0.4055

Standard Deviation

0.2225

0.185

Sample Variance

0.0495

0.034

Kurtosis

0.0178

0.506

Skewness

-1.32

-1.427

The above analysis explains the descriptive statistics of the log prices and the log return of the data. From the log return, we can observe that the mean value of log return is 0.3027, with a standard deviation of 0.185. The mean of log prices is 1.375 with the standard deviation of 0.2225. The skewness of the variable log returns is equal to -1.427, which is a negative value implying that the value of the log return is negatively skewed. The value of kurtosis of the log return is equal to 0.506, which is a positive value. This implies that the data of log return has a low distributed or low peaked about the mean. The skewness of the variable log price is equal to -1.32, which is a negative value implying that the value of the log return is negatively skewed. The value of kurtosis of the log return is equal to 0.0178, which is a positive value. This implies that the data of log return is low peaked about the mean.

b)

Stationary

The variables log returns and log prices are not stationary. These two variables, the log return and the log price, are transformed to make them stationary in the time series aspect. To evaluate the stationary, a time series plot is done on the series to indicate if they are stationary or not. It also helps in identifying which of the method can be used to transform the model in to a stationary model.

c)

ARIMA model is used in the following case to model the data

In these data, the univariate time series model that can be used in the modeling of the data is the ARIMA. In this case, the following process of modeling will be used.

ARIMA is often described as modeling time-series with an exogenous variable or as it’s called Auto Regressive moving average model with exogenous inputs (Barro and Sala-i-Martin 2012). They present several models of data analysis of time series when there are several time series in the process.

The first model present is very similar to a regression model for time series. The model equation takes the form:

{t} ~ N(0, 2)

In this model, Y is the response variable, and there are n predictors, each with t measurement points. Finally, time is added as a component that is regressed against, as if time was just another linear prediction variable.

A second model that is more in keeping with ARMA modeling is Vector Auto regression. A working conceptual definition could be multivariate regression of time series (Easterlin 2013). The equation to represent this model with i=1,…,t and j=1,...,k is:

{ij} ~ N(0,)

Or in matrix notation: . In this model we assume cov(si,tj) = ij for all s=t or 0 otherwise. However, again this model is not quite what is desired, as the representation is of all three variables as if they were of equal importance when forecasting. Our goal is to have a single response variable and multiple predictors working in conjunction with the usual ARIMA machinery.

First the trend analysis of the data is observed. The modeling of the time series involves the steps of model specification, model estimation, diagnostic checking. The statistical time series modeling techniques used in this study are the Exponential Smoothing Technique and Auto-Regressive Integrated Moving Average Technique.

In the selection of the appropriate technique for time series analysis, the smoothing of the data is done after ensuring the presence of trend. For smoothing, the common techniques discussed by Gardner (1985) are discussed below.

In the selection of ARIMA model, the stationary of the series is first checked and if the data is non-stationary, stationary is achieved by differencing technique. (Satya et al, 2007). The next processes are model identification, estimation and diagnostic checking. In time series analysis, an autoregressive integrated moving average (ARIMA) model is a generalization of an autoregressive moving average (ARMA) model. In theory, the most general class of models for forecasting a time series are stationary and can be made stationary by transformations such as differencing and logging. ARIMA models form an important part of the Box-Jenkins approach to time-series modeling. A non-seasonal ARIMA model is classified as an ARIMA (p, d, q) model, where: p is the number of autoregressive terms, d is the number of non-seasonal differences and q is the number of moving average terms.

(i) Model identification

Once we obtain a time series data the selection of the appropriate model is obtained by using Box and Jenkins two graphical procedures are used to access the correlation between the observations within a single time series data (Borts and stein 2014). Partial autocorrelation function and the correlation functions are used to check the characteristics of the data as described by Box and Jenkins. They clearly indicate the measure of association and relation of the data. The best class of ARIMA was selected is proposed by Box and Jenkins.

(ii) Estimation of parameters

The estimates of the coefficient of the ARIMA model are selected and at this stage. Different methods are used to obtain these estimates of the coefficients. Some of the methods used are the maximum likelihood method, the least square methods, and the methods of moments. Certain mathematical inequalities must be satisfied otherwise the coefficients are abandoned.

(iii) Diagnosis checks

Diagnostic checks are used to examine the statistical adequacy of the ARIMA model as it is being modeled. The residuals are examined to determine if the fitted model is adequate to fit the time series data in ARIMA. When the model fails to the diagnostic test its rejected and cannot be used to model the time series data (Conway, 2004). We repeat the cycle of identification, estimation, and diagnostic checking until we find a good final model.

The ARIMA model is obtained by taking Zt. as the first differenced time series, in this case d=1)

(Zt-u)-α1(Zt-1-u) -α2(Zt-2-u)-………………….αp (Zt.-p-u)+εt+β1εt-1+

β2εt-2+……………………..+βqεt-q

isreferred to as the ARIMA (p, 1,q) of order (p,q).

Different combinations of AR and MA individually yields different ARIMA models (Makridakis et al. 1998). The optimal model is obtained on the basis minimum value of Akaike Information Criteria (AIC) given by

AIC=-2logL+2m

Where m=p+q and L is the likelihood function. The root mean square error (RMSE) and the mean absolute percentage error (MAPE) have helped to evaluate the performance of the various approaches and are given below.

MAPE=1/n(∑|(Yt-Ft)/Yt|)

RMSE=√(1/n∑ (Yt-Ft)^2)

Where Yt is the milk production in different years and Ft is the forecasted milk production in the corresponding years and n is the number of years used as forecasting period.

d)

The CAPM model

The beta value for the share using the CAPM model specification ad the checking of the adequacy of the model has been examined. From the analysis of the CAPM model, it can be observed that the model account for 99.2% of the errors in the CAPM Model. It can also be observed that the Log return is significant since we can observe that there is t(238, 0.05)= 271.31 and the significant value equal to 0.000 which is significant less than the 0.05 level of confidence.

Log price = 1.01 + 1.20 log return

Predictor Coef SE Coef T P

Constant 1.01142 0.00157 644.80 0.000

log return 1.20037 0.00442 271.31 0.000

S = 0.0126576 R-Sq = 99.7% R-Sq(adj) = 99.7%

Analysis of Variance

Source DF SS MS F P

Regression 1 11.794 11.794 73611.09 0.000

Residual Error 238 0.038 0.000

Total 239 11.832

From the conclusion, it can be observed that the CAPM model is significant to the financial data as the model account for almost 100% of the errors in the model. The CAPM model is significant since it have a f (1, 238)= 73611.09 with a p- value of 0.000 which is less than 0.05 level of confidence. This implies that there is significant relationship

e)

From the analysis of the market using the CAPM model, it can be observed that the market price is stationary and hence cannot fall in either of the bear market nor the bull market. This is because the bear market is the market which seen to be declining. But from the CAPM model it can be observed that the market is a stationary market. This means that the market price is stationary and hence does not fall between the bear and the bull market for the period 2000 to December 2007.

Reference

Conway, M. (2004). Collecting Data with Electronic Tools. Washington, DC: ASTD.

Gardner, E.S., Jr. (1985). Exponential smoothing: The state of the art, Journal of Forecasting, 4,

1-28.

Satya Pal, Ramasubramanian, V and Mehta, S.C., 2007, Statistical models for Forecasting Milk

Production in India, J.Ind.Soc.Agril.Statist, 61(2), 2007: 80-83.

Borts ans stein (2014). Economic growth in the free market. The Economic Journal Vol. 75, No. 300

(Dec., 1965), pp. 822-824

Easterlin (2013), Will raising the incomes of all increase the happiness of all?; Journal of

Economic Behavior and Organization Vol. 35-47

Barro and Sala-i-Martin (2012). "Economic Growth and Convergence across the United States."

Working Paper 3419. Cambridge, Mass.: National Bureau of Economic Research (August)

Read

More

sponsored ads

Save Your Time for More Important Things

Let us write or edit the assignment on your topic

"Financial Econometrics - Descriptive Statistics and the Graph of Log Return and Log Prices"

with a personal 20% discount.

GRAB THE BEST PAPER