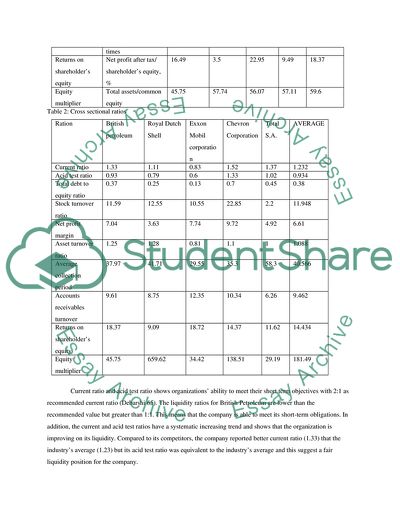

Cite this document

(Financial ratios, common size income statements and DuPont system Coursework, n.d.)

Financial ratios, common size income statements and DuPont system Coursework. https://studentshare.org/finance-accounting/1850388-financial-ratios-common-size-income-statements-and-dupont-system

Financial ratios, common size income statements and DuPont system Coursework. https://studentshare.org/finance-accounting/1850388-financial-ratios-common-size-income-statements-and-dupont-system

(Financial Ratios, Common Size Income Statements and DuPont System Coursework)

Financial Ratios, Common Size Income Statements and DuPont System Coursework. https://studentshare.org/finance-accounting/1850388-financial-ratios-common-size-income-statements-and-dupont-system.

Financial Ratios, Common Size Income Statements and DuPont System Coursework. https://studentshare.org/finance-accounting/1850388-financial-ratios-common-size-income-statements-and-dupont-system.

“Financial Ratios, Common Size Income Statements and DuPont System Coursework”. https://studentshare.org/finance-accounting/1850388-financial-ratios-common-size-income-statements-and-dupont-system.