StudentShare

Our website is a unique platform where students can share their papers in a matter of giving an example of the work to be done. If you find papers

matching your topic, you may use them only as an example of work. This is 100% legal. You may not submit downloaded papers as your own, that is cheating. Also you

should remember, that this work was alredy submitted once by a student who originally wrote it.

✕

Free

The Capital Asset Pricing Model - Report Example

Summary

The paper "The Capital Asset Pricing Model" highlights that a specific company may have different betas depending on the method used in computing it. For example, if the market proxy were the NASDAQ (which should be more appropriate here), the beta figure will be different…

- Subject: Macro & Microeconomics

- Type: Report

- Level: Masters

- Pages: 5 (1250 words)

- Downloads: 0

- Author: margaritafranec

Extract of sample "The Capital Asset Pricing Model"

Corporate Investment Analysis CAPM: Apple and Microsoft The capital asset pricing model (CAPM) is a pioneering model of asset pricing under uncertainty. First developed by a financial economist, William Sharpe (1964), later a winner of the Nobel Prize in economics, and Lintner (1965), the model establishes the link between risk and return on assets based on Markowitzs fundamental portfolio framework The model predicts that the expected return on assets is equal to the sum of the return on risk-free assets and the product of the beta of the asset and the expected return on the market portfolio.

In his book published in 1970, Mr. Sharpe stated that investment is subject to two types of risk: systematic risk and unsystematic risk. Unsystematic risks , otherwise known as “specific” risks are unique to individual stocks and can be lessened through diversification – that is, as the investor increases his holdings in his portfolio, his risks diminish. On the other hand, systematic risks are those that cannot be diversified away because all investments are affected - by such factors, for example, as interest rates, inflation and recession. It is the systematic risk that is correlated with the movement of the general market. Diversification does not solve the problem of systematic risk, so that during recessions the general market may move south and along with it the individual stocks that compose that market.

The CAPM formula which describes the relationship between risk and expected returns, is expressed by the following formula:

E(Ri) = Rf + im (E (Rm) – Rf)

Where:

E (Ri) is the expected return on lthe capital asset

Rf is the risk-free rate of interest

im (the beta coefficient) the sensitivity of the asset to market returns

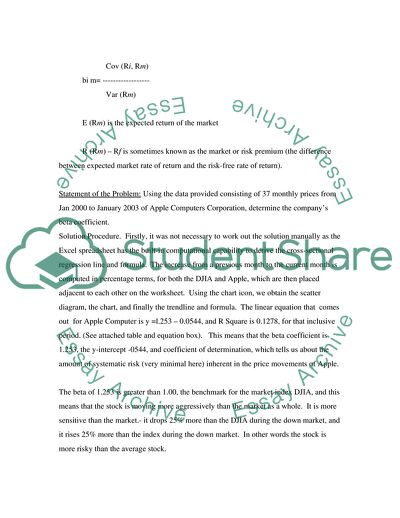

Cov (Ri, Rm)

= ------------------

Var (Rm)

E (Rm) is the expected return of the market

R (Rm) – Rf is sometimes known as the market or risk premium (the difference between expected market rate of return and the risk-free rate of return).

Statement of the Problem: Using the data provided consisting of 37 monthly prices from Jan 2000 to January 2003 of Apple Computers Corporation, determine the company’s beta coefficient.

Solution Procedure. Firstly, it was not necessary to work out the solution manually as the Excel spreadsheet has the built-in computational capability to derive the cross-sectional regression line and formula. The increase from a previous month to the current month is computed in percentage terms, for both the DJIA and Apple, which are then placed adjacent to each other on the worksheet. Using the chart icon, we obtain the scatter diagram, the chart, and finally the trendline and formula. The linear equation that comes out for Apple Computer is y =l.253 – 0.0544, and R Square is 0.1278, for that inclusive period. (See attached table and equation box). This means that the beta coefficient is 1.253, the y-intercept -0544, and coefficient of determination, which tells us about the amount of systematic risk (very minimal here) inherent in the price movements of Apple.

The beta of 1.253 is greater than 1.00, the benchmark for the market index DJIA, and this means that the stock is moving more aggressively than the market as a whole. It is more sensitive than the market.- it drops 25% more than the DJIA during the down market, and it rises 25% more than the index during the down market. In other words the stock is more risky than the average stock.

The website http://finance.yahoo.com/q/cq?d=v1&s=AAPL+beta , particularly the Profile thereof, states, unfortunately, that Apple’s beta is not available. Item 10 :”BETA N/A N/A 0.00 0.00% 0 Chart, , More” The Microsoft beta also is not available (http://finance.yahoo.com /q/pr?s=MSFT)

The 10 year Treasury Note is at 3.75% and this can be assumed as the risk-free rate. If the market rate of return is 12%, it means that the premium is (12-3.75) or 8.25%. In the absence of sourced data, let us assume that Microsoft has a beta of 1 (unity), it will show the following results by using the linear equation:

Y = 3.75 + 8.25(1) = 12.00

For Apple Computer which has a beta coefficient of 1.253, the equation will be:

Y = 3.75 + 8.25(1.253) = 3.75 + 10.33725 = 14.09%

Thus Apple Computer will yield 14.09 % return when the market as a whole makes 12%.

Why are betas different? Betas differ to the extent that they are sensitive to the movements of the market index such as the Dow Jones Industrial Average. Companies with a beta of greater than 1 are considered relatively aggressive, those with betas of less than 1 are defensive, while those than move in tandem with the market with 1 are considered neutral.

As between two companies, their betas differ because they are subject to different unsystematic risks – risk that are specific to the company and its industry, the risks it faces as it operates as a going concern. A lot of events – such as the discovery of a new product that becomes popular with the consumers, a marketing program that fails, corporate fraud, and many others – are unique to particular company and does not partake of the macro factors that affect the economy as a whole, factors that move the general market as represented by the market index. It is only through diversification that the unsystematic risks are reduced, if not eliminated.

A specific company may have different betas depending on the method used in computing it. For example, if the market proxy were the NASDAQ (which should be more appropriate here because both Microsoft and Apple are NASDAQ stocks), the beta figure will be different. Also different results would emerge if the NYSE Composite Index, or the S&P 500, or the Wilshire 5000 were used. Another reason is the length of historical data used as well as the time interval (weekly – used by Value Line, or monthly- used by Merrill Lynch).

The adjusted tables and linear regression graph for the DJIA and Apple Computers are shown below:

djia

apple

djia

apple

Date

Adj. Close*

Rtrn

Adj. Close*

Rtrn

Adj.rtrn

Adj.retrn

3-Jul

9,040.95

0.006178

19.09

0.001574

0.617777

0.157398

3-Jun

8,985.44

0.015274

19.06

0.061838

1.527413

6.183844

3-May

8,850.26

0.043652

17.95

0.262307

4.365166

26.23066

3-Apr

8,480.09

0.061055

14.22

0.005658

6.105506

0.565771

3-Mar

7,992.13

0.012806

14.14

-0.05796

1.28056

-5.79614

3-Feb

7,891.08

-0.02021

15.01

0.045265

-2.02053

4.526462

3-Jan

8,053.81

-0.0345

14.36

0.002094

-3.4504

0.209351

2-Dec

8,341.63

-0.06233

14.33

-0.07548

-6.23263

-7.54839

2-Nov

8,896.09

0.059433

15.5

-0.03547

5.943292

-3.54698

2-Oct

8,397.03

0.106047

16.07

0.108276

10.60468

10.82759

2-Sep

7,591.93

-0.12369

14.5

-0.01695

-12.3688

-1.69492

2-Aug

8,663.50

-0.00837

14.75

-0.03342

-0.83671

-3.34207

2-Jul

8,736.60

-0.05482

15.26

-0.13883

-5.48181

-13.8826

2-Jun

9,243.30

-0.06871

17.72

-0.23948

-6.87133

-23.9485

2-May

9,925.30

-0.0021

23.3

-0.03997

-0.21013

-3.9967

2-Apr

9,946.20

-0.04399

24.27

0.025349

-4.39931

2.534854

2-Mar

10,403.90

0.029467

23.67

0.090783

2.946735

9.078341

2-Feb

10,106.10

0.01876

21.7

-0.12217

1.876008

-12.2168

2-Jan

9,920.00

-0.01014

24.72

0.128767

-1.01381

12.87671

1-Dec

10,021.60

0.017256

21.9

0.028169

1.725608

2.816901

1-Nov

9,851.60

0.085564

21.3

0.212984

8.55638

21.29841

1-Oct

9,075.10

0.025713

17.56

0.132173

2.571319

13.21728

1-Sep

8,847.60

-0.11078

15.51

-0.16388

-11.0776

-16.3881

1-Aug

9,949.80

-0.05445

18.55

-0.01277

-5.44532

-1.27728

1-Jul

10,522.80

0.001942

18.79

-0.19183

0.194241

-19.1828

1-Jun

10,502.40

-0.03753

23.25

0.165414

-3.75278

16.54135

1-May

10,911.90

0.016479

19.95

-0.21734

1.647881

-21.734

1-Apr

10,735.00

0.08667

25.49

0.154961

8.667045

15.49615

1-Mar

9,878.80

-0.05874

22.07

0.209315

-5.87406

20.93151

1-Feb

10,495.30

-0.03601

18.25

-0.15587

-3.60141

-15.5874

1-Jan

10,887.40

0.009214

21.62

0.452957

0.921394

45.2957

Dec-00

10,788.00

0.035863

14.88

-0.09818

3.586346

-9.81818

Nov-00

10,414.50

-0.05073

16.5

-0.15644

-5.07333

-15.6442

Oct-00

10,971.10

0.030063

19.56

-0.24039

3.006319

-24.0388

Sep-00

10,650.90

-0.05031

25.75

-0.57745

-5.03072

-57.7453

Aug-00

11,215.10

0.065872

60.94

0.19937

6.587151

19.93702

Jul-00

10,522.00

0.007092

50.81

-0.02997

0.709233

-2.99733

Jun-00

10,447.90

-0.00707

52.38

0.247143

-0.70707

24.71429

May-00

10,522.30

-0.01971

42

-0.32291

-1.97132

-32.2908

Apr-00

10,733.90

-0.01721

62.03

-0.08659

-1.72131

-8.65852

Mar-00

10,921.90

0.078355

67.91

0.184959

7.835471

18.4959

Feb-00

10,128.30

-0.07424

57.31

0.104665

-7.42379

10.46646

Jan-00

10,940.50

51.88

REFERENCES

Brealey, RA, Myers, SC & Marcus, AJ, (1995). Fundamentals of Corporate Finance, , Boston, Mass: McGraw-Hill

Hirt, GA, & Block, SB (1987). Fundamentals of Investment Management, 2nd ed, Homewood IL: Irwin,

Meir. S, “Betas compared: Merrill Lynch vs. Value Line,” Journal of Portfolio Management 7, no. 2, winter 1981, pp. 41-44.

Van Horne, JC (1983). Financial management and policy, 2nd ednEnglewood Cliffs, NJ.: Prentice-Hall,

Read

More

sponsored ads

Save Your Time for More Important Things

Let us write or edit the report on your topic

"The Capital Asset Pricing Model"

with a personal 20% discount.

GRAB THE BEST PAPER